Emptying Your NS&I Account? If you’ve been thinking about emptying your NS&I account, pause before you hit withdraw. There’s a two-word warning floating around that could cost you big if you don’t take it seriously. NS&I (National Savings & Investments) has been the go-to place for safe, government-backed savings in the UK for decades. But making the wrong move at the wrong time—especially under pressure—could mean losing interest, missing prize draws, or worse, falling for a scam. Let’s break it all down in plain language. We’ll explore the risks, the meaning of this “two-word warning,” and what smart savers can do to avoid costly mistakes. Whether you’re a seasoned professional managing wealth or a 10-year-old learning about saving for the first time, this guide is here to make money talk clear, practical, and trustworthy.

Emptying Your NS&I Account?

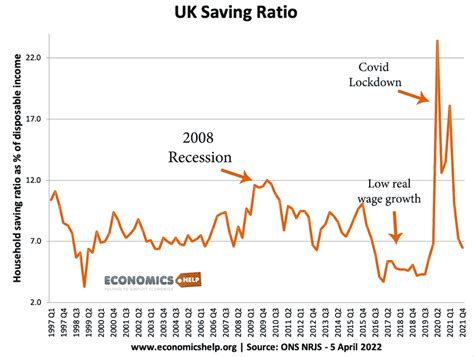

Emptying your NS&I account might feel like the smart move in a world of rising rates and flashy bank ads. But those two little words—“Act Now”—can cost you big. From scam risks to lost interest and weaker protection outside NS&I, the dangers are real. Instead of rushing, slow down, compare, and make a plan that fits your long-term goals. Remember: NS&I isn’t just another savings option—it’s one of the safest homes for your money in the UK.

| Point | Details |

|---|---|

| Topic | Emptying your NS&I account: risks, penalties, scams, and safe alternatives |

| Two-Word Warning | “Act Now” – a scam trigger phrase and risky advice |

| Interest Loss | Early withdrawals from fixed-term products may cost hundreds in lost interest |

| Government Backing | NS&I is 100% backed by HM Treasury, safer than bank FSCS (£85,000 cap) |

| Scam Risk | Rising phishing scams targeting NS&I customers |

| Official Source | NS&I Official Website |

A Quick History of NS&I (Why Brits Trust It)

NS&I has been around since 1861, originally created to encourage ordinary Brits to save. Back then, it was called the “Post Office Savings Bank.” Over time, it grew into a trusted institution used by millions. Fast forward to today, and NS&I manages over £200 billion of savings. Unlike banks, it doesn’t chase profits—it helps fund government borrowing in a safe way.

That’s why grandparents often buy Premium Bonds for grandkids, and why cautious savers prefer NS&I over shiny new fintech apps. It’s about trust.

What Does “Emptying Your NS&I Account” Really Mean?

When you empty your NS&I account, you withdraw all the money you’ve saved—whether it’s from Premium Bonds, Income Bonds, Direct Saver accounts, or fixed-term certificates. Sounds simple, right? But timing matters.

Imagine this: You’ve locked in money at 5% for two years. Six months later, another bank advertises 5.25%. Tempting, yes. But if you cash out early, you might lose a big chunk of earned interest. After fees, you’d probably be worse off.

The “Two-Word Warning” Explained If You’re Emptying Your NS&I Account

The phrase often used is “Act Now.” It shows up in scam texts, phishing emails, or even urgent-sounding ads. The goal? To make you panic.

- Scammers: They’ll say “Act Now” to protect your funds, asking you to transfer to a “safe account.” Spoiler: it’s fake.

- Misleading advice: Even friends or blogs can push urgency, making savers chase small gains without considering penalties.

That little phrase can cause big losses when it overrides calm, careful decision-making.

Real-Life Examples

- Scam Trap: In 2023, UK Finance reported over £1.2 billion lost to fraud, with investment scams being the most damaging. NS&I had to issue warnings about fake bond offers circulating online.

- Lost Interest: A saver with £20,000 in a 3-year NS&I bond who withdrew just 6 months early lost £600+ in penalties and forfeited future gains. That’s money gone for nothing.

- Missed Prizes: Premium Bond holders who emptied accounts days before a draw missed out on prize wins. NS&I data shows around £80 million in unclaimed prizes at any given time—often from people who pulled out too soon.

Why NS&I Is Safer Than Most Banks?

Here’s the big difference: backing.

- NS&I: Every penny is 100% guaranteed by HM Treasury.

- Banks: Only the first £85,000 per person per institution is protected under FSCS.

That means if you’ve got a large stash, pulling it out of NS&I and putting it in an ordinary bank could increase your risk, not reduce it.

During the 2008 financial crisis, when banks collapsed left and right, NS&I remained rock-solid. That’s why many professionals keep at least part of their “safe money” here.

Risks of Emptying Your Account Too Soon

1. Loss of Interest

Fixed-term products penalize early withdrawals. Cashing out too soon could wipe out hundreds.

2. Missed Premium Bond Prizes

Premium Bonds are a national favorite. Returns average 4.65% (2025), but you only win if you stay in the game. Empty before the draw? Your chance vanishes.

3. Scam Exposure

Scammers often target people moving large sums. One click on a fake link could mean goodbye to your life savings.

4. Reinvestment Risk

Chasing slightly higher rates elsewhere can backfire after taxes, fees, or changes in policy.

NS&I vs Banks vs Fintechs: A Quick Comparison

| Feature | NS&I | High-Street Bank | Challenger Bank / Fintech |

|---|---|---|---|

| Safety | 100% Treasury-backed | £85k FSCS limit | £85k FSCS limit |

| Typical Rates (2025) | 4–5% | 3–4% | 4–5.25% |

| Risks | Very Low | Moderate | Higher (newer players) |

| Extras | Premium Bond prizes | Full banking services | Mobile-first perks |

Step-by-Step Guide: What To Do Before Emptying Your NS&I Account?

Step 1: Check Your Product Type

- Premium Bonds = no penalty, but prize chances stop.

- Easy Access = flexible, but check rates.

- Fixed-Term = expect penalties if you leave early.

Step 2: Compare Rates Properly

Use trusted sites like MoneySavingExpert or Bank of England stats. Don’t rely on ads alone.

Step 3: Watch for Scams

NS&I will never cold-call. If you’re told “move money now,” hang up.

Step 4: Think Long-Term

Ask: Am I saving for retirement, a house, or emergencies? Each goal demands a different approach.

Actionable Tips for Savers

- Diversify: Don’t keep everything in NS&I, but don’t abandon it either. Split savings.

- Use Tax Allowances: Make the most of your Personal Savings Allowance (£1,000 for basic-rate taxpayers).

- Plan Withdrawals: If you need money, schedule withdrawals right after interest is paid or draws are made.

- Review Annually: Check your accounts every 6–12 months. Interest rates shift quickly.

Starting October, Parking at Home Could Cost You; The New Driveway Charge Explained

When It Does Make Sense to Empty Your NS&I Account?

Sometimes, emptying your account is the right move:

- You’re buying a home and need liquid cash.

- You’ve hit your financial target (e.g., retirement).

- You want to diversify into other assets like pensions, ISAs, or investments.

The key is planning, not panic.